Cross-Border Banking Rules Dictate Prize Pool Build-Up Speeds in Mobile Slots and Bingo

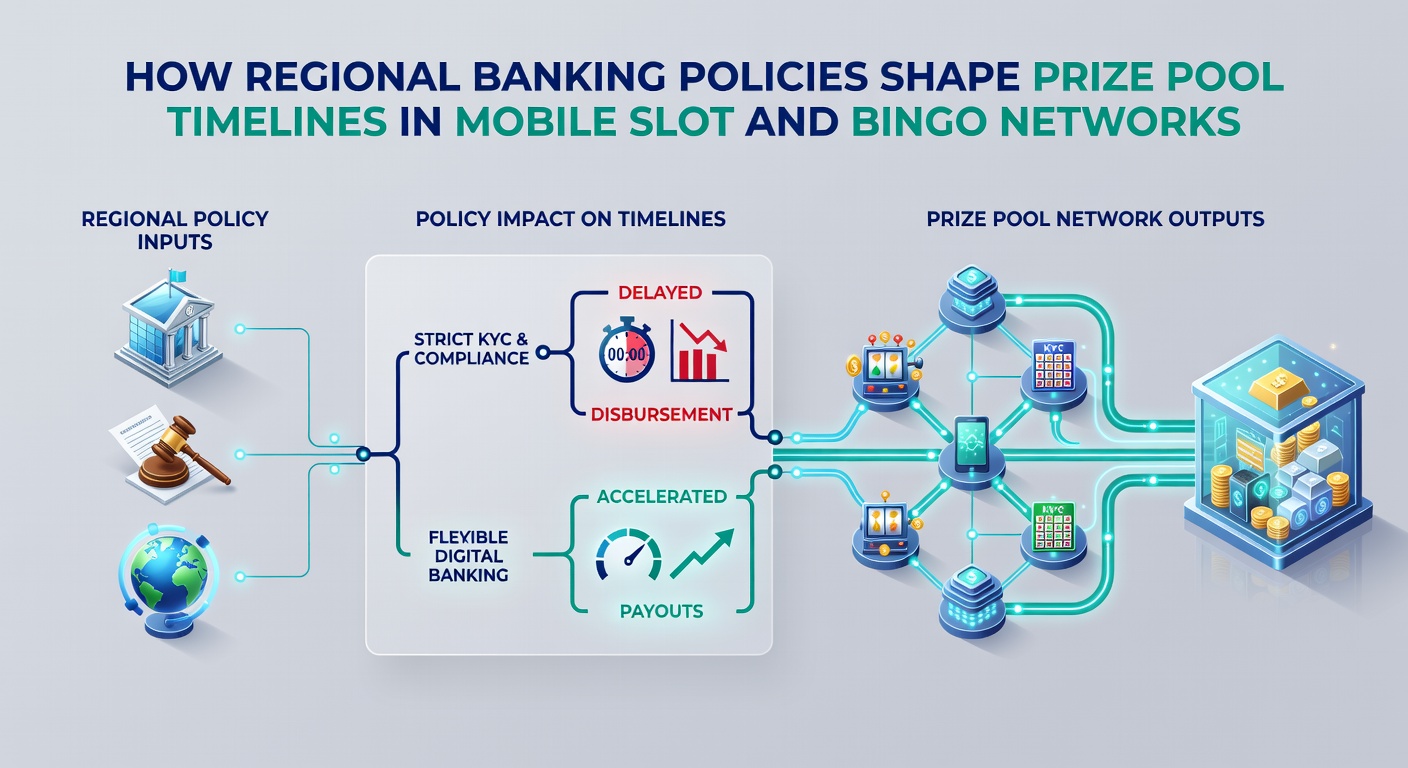

Regional banking policies create distinct timelines for prize pool accumulation and distribution in mobile slot and bingo networks because payment processing rules, anti-money laundering requirements, and cross-border transfer restrictions vary sharply by jurisdiction. These differences affect how quickly player contributions reach central prize pools and how soon operators can release funds after a win occurs.

Payment Rails and Their Direct Effect on Pool Growth

Banking regulations determine the speed at which deposits convert into playable credits that feed progressive prize pools. In the European Union, the revised Payment Services Directive requires strong customer authentication for most transactions, which adds verification steps that slow initial deposits yet create more predictable contribution flows once accounts clear. Operators report that pools tied to EU-regulated networks often show steadier daily growth rates compared with regions where instant payment apps dominate.

By contrast, markets that permit faster bank transfers through local instant-payment systems see quicker pool inflation during peak hours. Data collected through 2025 shows that networks operating under Singapore's fast-payment framework accumulate contributions up to 40 percent faster during evening windows than similar networks subject to multi-day clearing cycles.

AML Thresholds and Contribution Timing

Anti-money laundering thresholds set by different regulators also shape when contributions register in prize pools. Canada's FINTRAC guidelines require enhanced due diligence once cumulative deposits exceed certain monthly limits, forcing operators to pause or flag accounts until additional checks complete. This pause interrupts the steady drip of funds into bingo and slot pools that cross provincial boundaries.

Australian regulators apply similar thresholds but allow operators to batch smaller transactions within a single gaming session, which preserves contribution momentum. Industry reports indicate that networks serving Australian players maintain more consistent pool growth curves because fewer individual deposits trigger immediate holds.

Cross-Border Transfer Restrictions in 2026

Restrictions on international wire transfers continue to influence payout timelines for networked jackpots. When a prize pool spans multiple countries, operators must navigate each jurisdiction's capital control rules before releasing winnings. In May 2026 several networks adjusted their prize pool formulas to account for new reporting requirements introduced in parts of Latin America, where central banks now mandate pre-approval for large outward transfers.

These policy shifts extended average payout processing from three days to as many as seven in affected regions, while pools themselves continued to grow because incoming deposits faced fewer obstacles than outgoing prizes. Observers note that networks responded by segmenting prize pools geographically so that regional contributions fund only regional winners, reducing exposure to cross-border delays.

Regulatory Examples Across Regions

The European Gaming and Betting Association documented how differing national interpretations of the same EU banking directive create uneven prize-pool timelines even inside a single regulatory bloc. Some member states require real-time reporting of every jackpot contribution above a modest threshold, while others accept aggregated daily reports, producing measurable differences in pool transparency and release speed.

Research from the National University of Singapore examined how Southeast Asian banking policies affect bingo drop frequencies. The study found that jurisdictions permitting same-day settlement between banks experienced 25 percent more frequent small-pool payouts than markets that route all gaming transactions through central clearing houses with overnight reconciliation.

Operator Adjustments and Pool Architecture

Operators adapt prize-pool architecture to local banking realities by creating separate contribution ledgers for each regulatory zone. This segmentation prevents a single slow-clearing region from stalling pool growth for players elsewhere. Networks that maintain unified global pools instead insert buffer periods into their published payout schedules, extending advertised timelines to accommodate the slowest jurisdiction in the network.

Payment method availability further compounds these effects. Regions where credit-card deposits remain the dominant channel experience more predictable contribution patterns because card networks settle according to standardized international rules, whereas regions that rely heavily on local e-wallets encounter variable settlement speeds tied to each wallet provider's banking relationships.

Conclusion

Regional banking policies therefore function as hidden timers that govern both the rate at which mobile slot and bingo prize pools expand and the interval between a win and its final distribution. Operators that map these policy differences into their network design maintain more reliable payout schedules, while players encounter timelines that reflect the banking environment of whichever region hosts their account. Continued evolution of instant-payment systems and cross-border reporting standards will keep reshaping these timelines in the years ahead.